Measure Volume, Momentum, Trend, VolatilityThis script displays the following indicators in one pane to quickly determine several important factors regarding price action. It allows the user to quickly see all of most important factors surrounding price action in one pane with one quick glance. This should be incredibly helpful and allow things like double divergence and trend confirmation to be spotted much more quickly. I personally use the data in this indicator to replace four separate indicators and it has brought my win rate and profit factor significantly higher. I hadn't seen any place where all of the best J. Welles Wilder indicators such as RSI, Parabolic SAR, and DMI/ADX were brought into one easy to use interface. This is my attempt at fixing that gap. For a much deeper understanding of how to use these indicators, I recommend reading New Concepts in Technical Trading Systems written by J. Welles Wilder.

Momentum via RSI (Relative Strength Index)

Volume via MFI (Money Flow Index)

Volatility via DMI/ADX (Direction Movement Index/Average Directional Index)

Trend via Parabolic SAR (Parabolic Stop and Reverse)

It is worth noting that DMI/ADX and Parabolic SAR can both help determine trend strength and volatility.

The Volatility mechanism is measured by DMI and ADX and displayed at the top of the pane using circles. The top, tiny circles reflect if show if positive DI or negative DI has a higher value. The small circles directly underneath indicate whether or not the ADX is above 20 (configurable, some may choose to increase this to 25 or even 30).

The Momentum mechanism is shown as standard RSI with the default being a white line and default period of 14, which is all configurable.

The Volume mechanism is shown as standard MFI with the default being a fuchsia line and default period of 14, which is also configurable.

The momentum and volume oscillators should be used in conjunction to help spot whether the trend is strong or weak using divergences and the middle, overbought, and oversold levels. These levels are also configurable.

The Trend mechanism is measured by Parabolic SAR and displayed at the bottom of the pane using diamonds. The default is red diamonds when in a bear trend, green when in an uptrend which is configurable. When price is above the Parabolic SAR, it is considered to be an uptrend. When price is below the Parabolic SAR, it is considered to be a downtrend. The way price is measured is also configurable (i.e. open, close, ohlc4, hlc3, etc.). When price crossed above or below the Parabolic SAR, the diamonds will change colors.

All the indicators displayed should be used in a well rounded strategy. For instance, I only trade when ADX is above 20 and rarely trade against the trend shown via PSAR. When trend shifts and divergences helped indicate a trend shift would occur using the RSI and MFI, it can be a great spot to take an entry. RSI/MFI can also confirm the trend is strong when they are not showing divergences and inline with price action. All of this data should be used in conjunction with good fundamental data and technical levels. Divergences with RSI and MFI on double tops or bottoms can also be incredibly powerful. There is no right or wrong way to use all the data displayed in this indicator, however using all four pillars of trading (Momentum, Volume, Trend, Volatility) will help ensure only the best trades are taken.

Cari dalam skrip untuk "profit factor"

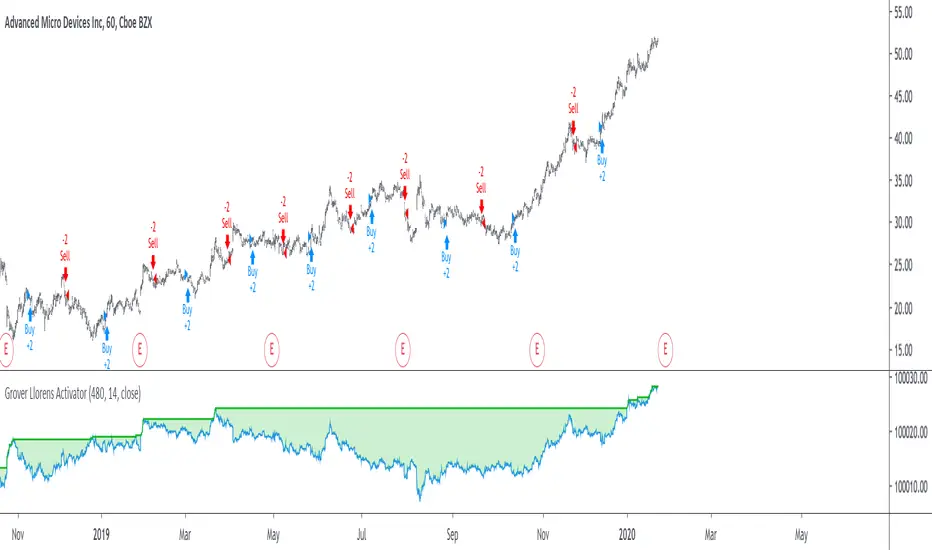

Grover Llorens Activator Strategy AnalysisThe Grover Llorens Activator is a trailing stop indicator deeply inspired by the parabolic SAR indicator, and aim to provide early exit points and reversal detection. The indicator was posted not so long ago, you can find it here :

Today a strategy using the indicator is proposed, and its profitability is analyzed on 3 different markets with the main time frame being 1 hour, remember that lower time frames involve lower absolute price changes, therefore we are way more affected by the spread, and we can require a larger position sizing depending on our investment target, trading higher time-frames is always a good practice and this is why 1 hour is selected. Based on the result we might make various conclusions regarding the indicator accuracy and might have ideas on future improvements of the indicator.

I'am not great when it comes to strategy design, i still hope to share correct and useful information in this post, let me know your thoughts on the post format and if i should make more of these.

Setup And Rules

The analysis is solely based on the indicator signals, money management isn't taken into account, this allow us to have an idea on the indicator robustness and resilience, particularly on extremely volatile markets and ones exhibiting a chaotic structure, altho it is normally good practice to close any position before a market closure in order to avoid any potential major gaps.

The settings used are 480 for length and 14 for mult, this create relatively mid term signals that are suited for a trend indicator such as the Grover Llorens Activator, unfortunately we can't infer the indicator optimal settings, thats how it is with any technical indicator anyway.

Here are the rules of our strategy :

long : closing price cross over the indicator

short : closing price cross under the indicator

We use constant position sizing, once a signal is triggered all the previous positions are closed.

Description Of The Statistics Used

Various statistics are presented in this post, here is a brief description of the main ones :

Percent Profitability (higher = better): Percentage of winning trades, that is : winning trades/total number of trades × 100

Maximum Drawdown (lower = better) : The highest difference between a peak and a valley in the balance, that is : peak - valley , in percentage : (peak - valley)/peak × 100

Profit Factor (higher = better) : Gross profit divided by gross loss, values under 1 represent gross losses superior to the gross profits

Remember that more volatility = more risk, since higher absolute price changes can logically cause larger losses.

EURUSD

The first market analyzed is the Forex market with the EURUSD major pair with a position sizing of 1000 units (1 micro lot). Since October EURUSD is not showing any particular strong trend but posses a discrete rising motion, fortunately cycles can be observed.

The equity was rising until two trades appeared causing a decline in the equity. Before October a bearish market could be observed.

We can see that the equity is rising, the trend still posses various retracements that affect our indicator, however we can see that the indicator totally nail the end of the trend, thats the power of converging toward the price.

In short :

$ 86.63 net profit

340 closed trades

37.65 % profitable (thats a lot of loosing trades)

1.19 profit factor

$ 76.67 max drawdown

Applying a spread would create negative results (in general the average spread is used), not a great start...

BTCUSD

The cryptocurrency market is relatively more volatile than others, which also mean potentially higher returns, we test the indicator using certainly the most traded cryptocurrency, BTCUSD. We will use a position sizing of 1 unit.

In the case of BTCUSD the strategy balance is relatively stationary around the initial capital, with of course high dispersion.

from september to december the market is bearish with various ranging periods, no apparent cycles can be observed, except maybe in the ranging period of october, this ranging period is followed by a non linear trend (relatively parabolic) that the indicator failed to capture in its integrity (this is a recurrent problem and it is starting to piss me off xD).

In short :

$ 2010.64 net profit (aka how i bet the crypto market)

395 closed trades

38.23 % profitable

1.036 profit factor

$ 5738.01 max drawdown (aka how i lost to the crypto market)

AMD

AMD stand for Advanced Micro Devices and is a company focused on the development of computer technology, i love the microprocessor market and i really like AMD who start this year in a pretty great way with a net bullish trend.

The performance of the indicator on AMD is decent (at last !) with the equity producing many new higher highs. The indicator performance still drop in the middle end of 2019 with a large equity drawdown of 17$ caused by the gap of august 8. Unfortunately AMD, like lot of well behaving stocks can only tells us that the indicator has good performances on heavily trending markets with no excess of noise or chaotic structures.

In short :

$ 17.86 net profit (Enough for a consistent lunch)

295 closed trades

36.27 % profitable

1.414 profit factor

$ 10.37 max drawdown.

Conclusion

A strategy using the recently proposed Grover Llorens activator has been presented. We can easily conclude that the indicator can't possibly generate long term returns under chaotic and volatile markets, and could even produce unnecessary trades in trending markets without much parasitic fluctuations such as noise and retracements (think about a simple linear trend) since the indicator converge toward the price and would therefore automatically cross over/under the trend, thus guaranteeing a false signal.

However we have seen its ability to provide accurate early reversal detection shine from time to time, thus over performing lagging indicators in this aspect, however the duration of price fluctuations isn't fixed at a certain period, the rate of convergence should be way faster during volatile fluctuations, of moderate speed during more cyclic fluctuations, and really slow with apparent long term trends, this could be achieved by making the indicator adaptive, but it won't really make it necessarily perform better.

That said i still believe that converging trend indicators are really interesting and aim to capture the non lasting behavior of price fluctuations, they shouldn't receive so much hate (think about the poor p-sar).

Thanks for reading !

FFT Strategy Bi-Directional Stop/Profit/Trailing + VMA + AroonThis strategy uses the Fast Fourier Transform inspired from the source code of @tbiktag for the Fast Fourier Transform & @lazybear for the VMA filter.

If you are not familiar with the Fast Fourier transform it is a variation of the Discrete Fourier Transform. Veritasium on youtube has a great video on it with a follow up recommendation from 3brown1blue. In short it will extract all the frequencies from a set of data. @tbiktag laid the groundwork for creating the indicator which will allow you to isolate only those signals which are the most relevant and remove the noise. I recommend having @tbiktag's FFT Transform indicator side by side with this to understand what my variation is doing by setting similar settings .

Using this idea, you can then optimize a strategy to the frequencies that are best. The main entry signal is when the FFT Signal crosses above or below the 0 line .

Included with this strategy is the ability to optionally bi-directionally set:

Stop Loss

Trailing Stop Loss

Take Profit

Trailing Take Profit

Entries are optionally further filtered by use of the VMA using the algorithm from LazyBear which allows you to adjust a variable moving average with 3 market trend detections. Green represents upwards momentum; Blue sideways trading and Red downwards momentum. The idea being to filter out buy or sell entries unless the market is moving in that direction, and this makes a big difference as you can see for yourself when you turn it off or on. Turning it off will change the color of the FFT signal to orange instead of the green, blue, red colors .

I have added 2 custom stop loss types as well for experimentation:

1. VMA Filter stop loss to exit the trade if the VMA detects a market trend direction change matching the rules you have set. I have set this to off by default, but it is there so you can see what affect it may have on other tickers. It can increase the profit factor but usually at a cost of net profit.

2. The Aroon Filter stop loss with different lengths for the short or long direction. For the Aroon strategy (which is a trend change detector) it is considered bullish if the upper line (green in my code) is above 70 and the lower line (red in my code) is below 30 and the opposite for the bearish case. With this in mind, I have set it to filter by default only the extreme ends (99 and 1) to increase profit factor and net profit but I encourage you to try different settings and see how it affects things. Turning this off yields much higher net profit but at the cost of the profit factor and drawdown . To disable this just uncheck the 'Use Aroon Filter Long' (or short) and it will also hide the aroon graphics and crosses on the plot.

I will be adding more features in an attempt to lower the drawdown on this strategy but I hope you enjoy what I have so far!

Smoothed Heikin Ashi Trend on Chart - TraderHalai BACKTESTSmoothed Heikin Ashi Trend on chart - Backtest

This is a backtest of the Smoothed Heikin Ashi Trend indicator, which computes the reverse candle close price required to flip a Heikin Ashi trend from red to green and vice versa. The original indicator can be found in the scripts section of my profile.

This particular back test uses this indicator with a Trend following paradigm with a percentage-based stop loss.

Note, that backtesting performance is not always indicative of future performance, but it does provide some basis for further development and walk-forward / live testing.

Testing was performed on Bitcoin , as this is a primary target market for me to use this kind of strategy.

Sample Backtesting results as of 10th June 2022:

Backtesting parameters:

Position size: 10% of equity

Long stop: 1% below entry

Short stop: 1% above entry

Repainting: Off

Smoothing: SMA

Period: 10

8 Hour:

Number of Trades: 1046

Gross Return: 249.27 %

CAGR Return: 14.04 %

Max Drawdown: 7.9 %

Win percentage: 28.01 %

Profit Factor (Expectancy): 2.019

Average Loss: 0.33 %

Average Win: 1.69 %

Average Time for Loss: 1 day

Average Time for Win: 5.33 days

1 Day:

Number of Trades: 429

Gross Return: 458.4 %

CAGR Return: 15.76 %

Max Drawdown: 6.37 %

Profit Factor (Expectancy): 2.804

Average Loss: 0.8 %

Average Win: 7.2 %

Average Time for Loss: 3 days

Average Time for Win: 16 days

5 Day:

Number of Trades: 69

Gross Return: 1614.9 %

CAGR Return: 26.7 %

Max Drawdown: 5.7 %

Profit Factor (Expectancy): 10.451

Average Loss: 3.64 %

Average Win: 81.17 %

Average Time for Loss: 15 days

Average Time for Win: 85 days

Analysis:

The strategy is typical amongst trend following strategies with a less regular win rate, but where profits are more significant than losses. Most of the losses are in sideways, low volatility markets. This strategy performs better on higher timeframes, where it shows a positive expectancy of the strategy.

The average win was positively impacted by Bitcoin’s earlier smaller market cap, as the percentage wins earlier were higher.

Overall the strategy shows potential for further development and may be suitable for walk-forward testing and out of sample analysis to be considered for a demo trading account.

Note in an actual trading setup, you may wish to use this with volatility filters, combined with support resistance zones for a better setup.

As always, this post/indicator/strategy is not financial advice, and please do your due diligence before trading this live.

Original indicator links:

On chart version -

Oscillator version -

Update - 27/06/2022

Unfortunately, It appears that the original script had been taken down due to auto-moderation because of concerns with no slippage / commission. I have since adjusted the backtest, and re-uploaded to include the following to address these concerns, and show that I am genuinely trying to give back to the community and not mislead anyone:

1) Include commission of 0.1% - to match Binance's maker fees prior to moving to a fee-less model.

2) Include slippage of 10 ticks (This is a realistic slippage figure from searching online for most crypto exchanges)

3) Adjust account balance to 10,000 - since most of us are not millionaires.

The rest of the backtesting parameters are comparable to previous results:

Backtesting parameters:

Initial capital: 10000 dollars

Position size: 10% of equity

Long stop: 2% below entry

Short stop: 2% above entry

Repainting: Off

Smoothing: SMA

Period: 10

Slippage: 10 ticks

Commission: 0.1%

This script still remains to shows viability / profitablity on higher term timeframes (with slightly higher drawdown), and I have included the backtest report below to document my findings:

8 Hour:

Number of Trades: 1082

Gross Return: 233.02%

CAGR Return: 14.04 %

Max Drawdown: 7.9 %

Win percentage: 25.6%

Profit Factor (Expectancy): 1.627

Average Loss: 0.46 %

Average Win: 2.18 %

Average Time for Loss: 1.33 day

Average Time for Win: 7.33 days

Once again, please do your own research and due dillegence before trading this live. This post is for education and information purposes only, and should not be taken as financial advice.

STRATEGY TESTER ENGINE - ON CHART DISPLAY - PLUG & PLAYSo i had this idea while ago when @alexgrover published a script and dropped a nugget in between which replicates the result of strategy tester on chart as an indicator.

So it seemed fair to use one of his strategy to display the results.

This strategy tester can now be used in replay mode like an indicator and you can see what happen at a particular section of the chart which was is not possible in default strategy tester results of TV.

Please read how each result is calculated so you will know what you are using.

This engine shows most common results of strategy tester in a single screen, which are as follows:

1. Starting Capital

2. Current Profit Percentage

3. Max Profit Percentage

4. Gross Profit

5. Gross Loss

6. Total Closed Trades

7. Total Trades Won

8. Total Trades Lost

9. Percentage Profitable

10. Profit Factor

11. Current Drawdown

12. Max Drawdown

13. Liquidation

So elaborating on what is what:

1. Starting Capital - This stays 0, which signifies your starting balance as 0%. It is set to 0 so we can compare all other results without any change in variables. If set to 100, then all the results will be increased by 100. Some users might find it useful to set it to 100, then they can change code on line 41 from to and it should show starting balance as 100%.

2. Current Profit Percentage - This shows your current profit adjusted to current price of the candle, not like TV which shows after candle is close. There is a comment on the line 38 which can be removed and your can see unrealized profit as well in this section. Please note that this will affect Draw-down calculations later in this section.

3. Max Profit Percentage - This will show you your max profit achieved during your strategy run, which was not possible yet to see via strategy tester. So, now you can see how much profit was achieved by your strategy during the run and you can compare it with chart to see what happens during bull-run or bear-run, so you can further optimize your strategy to best suit your desired results.

4. Gross Profit - This is total percentage of profit your strategy achieved during entire run as if you never had any losses.

5. Gross Loss - This is total percentage of loss your strategy achieved during entire run as if you never had any profits.

6. Total Closed Trades - This is total number of trades that your strategy has executed so far.

7. Total Trades Won - This is the total number of trades that your strategy has executed that resulted in positive increase in equity.

8. Totals Trades Lost - This is the total number of trades that your strategy has executed that resulted in decrease in equity.

9. Percentage Profitable - This is the ratio between your current total winning trades divided by total closed trades, and finally multiplied by 100 to get percentage results.

10. Profit Factor - This is the ratio between Gross Profit and Gross Loss, so if profit factor is 2, then it indicates that you are set to gain 2 times per your risk per trade on average when total trades are executed.

11. Current Drawdown - This is important section and i want you to read this carefully. Here draw-down is calculated very differently than what TV shows. TV has access to candle data and calculates draw-down accordingly as per number of trades closed, but here DD is calculated as difference between max profit achieved and current profit. This way you can see how much percentage you are down from max peak of equity at current point in time. You can do back-test of the data and see when peak was achieved and how much your strategy did a draw-down candle by candle.

12. Max Drawdown - This is also calculated differently same as above, current draw-down. Here you can see how much max DD your strategy did from a peak profit of equity. This is not set as max profit percentage is set because you will see single number on display, while idea is to keep it custom. I will explain.

So lets say, your max DD on TV is 30%. Here this is of no use to see Max DD , as some people might want to see what was there max DD 1000 candles back or 10 candle back. So this will show you your max DD from the data you select. TV shows 25000 candle data in a chart if you go back, you can set the counter to 24999 and it will show you max DD as shown on TV, but if you want custom section to show max DD , it is now possible which was not possible before.

Also, now let's say you put DD as 24999 and open a chart of an asset that was listed 1 week ago, now on 1H chart max DD will never show up until you reach 24999 candle in data history, but with this you can now enter a manual number and see the data.

13. Liquidation - This is an interesting feature, so now when your equity balance is less than 0 and your draw-down goes to -100, it will show you where and at what point in time you got liquidated by adding a red background color in the entire section. This is the most fun part of this script, while you can only see max DD on TV.

------------------------------------------------------------------------------

How to Use -

1 word, plug and play. Yes. Actual codes start from line 33.

select overlay=false or remove it from the title in your strategy on first line,

Just copy the codes from line 33 to 103,

then go to end section of your strategy and paste the entire code from line 33 to line 103,

see if you have any duplicate variable, edit it,

Add to chart.

What you see above is very contracted view. Here is how it looks when zoomed in.

imgur.com

----------------------------------------------------------------------------------

Feel free to edit and share and use. If you use it in your scripts, drop me tag. Cheers.

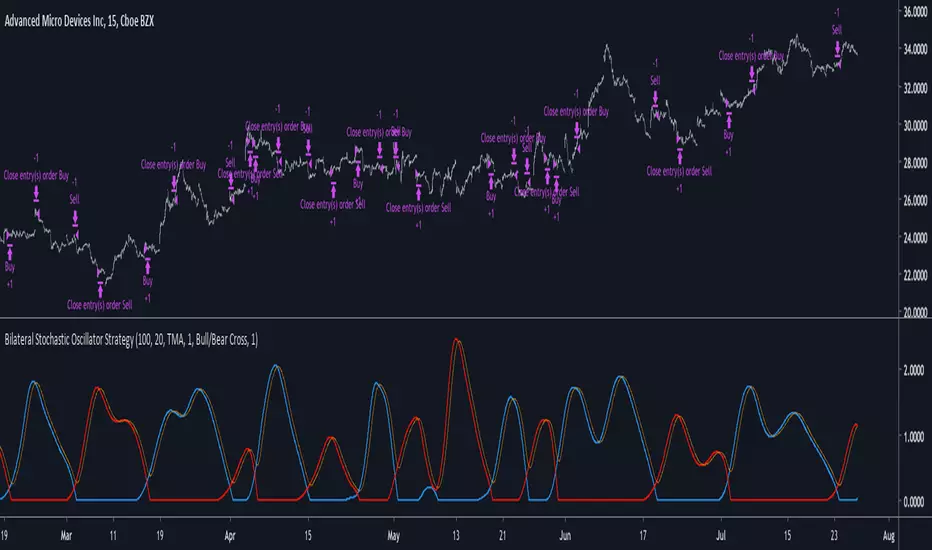

Bilateral Stochastic Oscillator StrategyIntroduction

Strategy based on the bilateral stochastic oscillator, this oscillator aim to detect trends and possible reversal points of the current trend. The oscillator is composed of 1 bull line in blue and 1 bear line in red as well as a signal line in orange, the strategy have many options such as two different strategy framework and a martingale mode. If you require more information about the indicator go check it into my uploaded indicators.

Strategy Frameworks

There are two frameworks available that can be selected from the strategy settings window. Both have the same closing conditions, the "Bull/Bear Cross" entry conditions are :

Buy : when the bull line cross over the bear line

Sell : when the bear line cross over the bull line

The "Signal Cross" entry conditions are :

Buy : when the bull line cross over the signal line

Sell : when the bear line cross over the signal line

Both have the same close conditions that is : close when bull/bear cross under the signal line.

Introduction To Martingale

The martingale money management system consist to double the order size after a loosing trade and can be described as a 2^x where x is the current number of loosing trades since the last win trade, when we win a trade the order size return to the default order size. Therefore our order size function is based on exponential growth.

This system enable the trader to win back his previous losses plus a potential profit, martingales must always be used with stops and sometimes take profits in order to get control in a strategy.

It must always be taken into account that in a series of losses the balance can exponentially decay thus ending to 0 in a matter of trades, this is why it is not recommended to use such system. The strategy allow you to select a martingale multiplier that can be inferior to 2 thus limiting risks, a multiplied of 1 disable the martingale.

Results

Those are the some statistics of the strategy applied to some forex majors by using the default settings in a time frames of 15 minutes.

//-------------------------------------------------------

EURUSD - Order Size 1000 - Spread 0.0002

Profit : $ 21.08

Trades : 19

PP : 57.89 %

Profit Factor : 3.228

Max Drawdown : -$ 3.81

Average Trade : $ 1.11

//-------------------------------------------------------

GBPUSD - Order Size 1000 - Spread 0.0002

Profit : $ 2.31

Trades : 20

PP : 55 %

Profit Factor : 0.938

Max Drawdown : -$ 20.29

Average Trade : $ 0.12

//-------------------------------------------------------

EURAUD - Order Size 1000 - Spread 0.0002

Profit : -$ 9.22

Trades : 20

PP : 40 %

Profit Factor : 0.698

Max Drawdown : -$ 23.44

Average Trade : $ 0.46

//-------------------------------------------------------

EURCHF - Order Size 1000 - Spread 0.0002

Profit : $ 1.58

Trades : 24

PP : 54.17 %

Profit Factor : 1.103

Max Drawdown : -$ 7.23

Average Trade : $ 0.07

//-------------------------------------------------------

Conclusions

Based on the results the strategy does not posses the sufficient performance in order to apply a martingale or any other growth systems as order size. Parameters might be subject to drastic changes depending on the market/time-frame in order to return long-term positive results. I let you draw your conclusions.

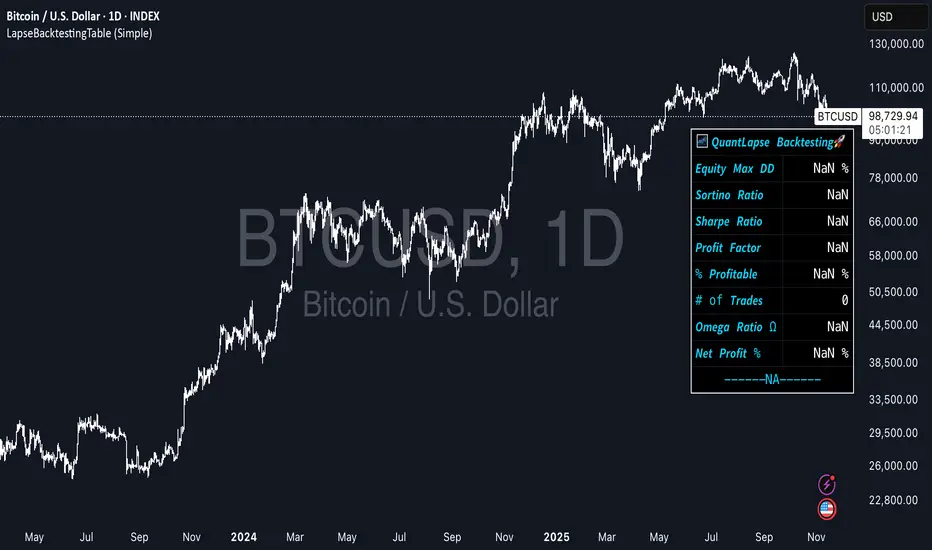

LapseBacktestingTableLibrary "LapseBacktestingMetrics"

This library provides a robust set of quantitative backtesting and performance evaluation functions for Pine Script strategies. It’s designed to help traders, quants, and developers assess risk, return, and robustness through detailed statistical metrics — including Sharpe, Sortino, Omega, drawdowns, and trade efficiency.

Built to enhance any trading strategy’s evaluation framework, this library allows you to visualize performance with the quantlapseTable() function, producing an interactive on-chart performance table.

Credit to EliCobra and BikeLife76 for original concept inspiration.

curve(disp_ind)

Retrieves a selected performance curve of your strategy.

Parameters:

disp_ind (simple string): Type of curve to plot. Options include "Equity", "Open Profit", "Net Profit", "Gross Profit".

Returns: (float) Corresponding performance curve value.

cleaner(disp_ind, plot)

Filters and displays selected strategy plots for clean visualization.

Parameters:

disp_ind (simple string): Type of display.

plot (simple float): Strategy plot variable.

Returns: (float) Filtered plot value.

maxEquityDrawDown()

Calculates the maximum equity drawdown during the strategy’s lifecycle.

Returns: (float) Maximum equity drawdown percentage.

maxTradeDrawDown()

Computes the worst intra-trade drawdown among all closed trades.

Returns: (float) Maximum intra-trade drawdown percentage.

consecutive_wins()

Finds the highest number of consecutive winning trades.

Returns: (int) Maximum consecutive wins.

consecutive_losses()

Finds the highest number of consecutive losing trades.

Returns: (int) Maximum consecutive losses.

no_position()

Counts the maximum consecutive bars where no position was held.

Returns: (int) Maximum flat days count.

long_profit()

Calculates total profit generated by long positions as a percentage of initial capital.

Returns: (float) Total long profit %.

short_profit()

Calculates total profit generated by short positions as a percentage of initial capital.

Returns: (float) Total short profit %.

prev_month()

Measures the previous month’s profit or loss based on equity change.

Returns: (float) Monthly equity delta.

w_months()

Counts the number of profitable months in the backtest.

Returns: (int) Total winning months.

l_months()

Counts the number of losing months in the backtest.

Returns: (int) Total losing months.

checktf()

Returns the time-adjusted scaling factor used in Sharpe and Sortino ratio calculations based on chart timeframe.

Returns: (float) Annualization multiplier.

stat_calc()

Performs complete statistical computation including drawdowns, Sharpe, Sortino, Omega, trade stats, and profit ratios.

Returns: (array)

.

f_colors(x, nv)

Generates a color gradient for performance values, supporting dynamic table visualization.

Parameters:

x (simple string): Metric label name.

nv (simple float): Metric numerical value.

Returns: (color) Gradient color value for table background.

quantlapseTable(option, position)

Displays an interactive Performance Table summarizing all major backtesting metrics.

Includes Sharpe, Sortino, Omega, Profit Factor, drawdowns, profitability %, and trade statistics.

Parameters:

option (simple string): Table type — "Full", "Simple", or "None".

position (simple string): Table position — "Top Left", "Middle Right", "Bottom Left", etc.

Returns: (table) On-chart performance visualization table.

This library empowers advanced quantitative evaluation directly within Pine Script®, ideal for strategy developers seeking deeper performance diagnostics and intuitive on-chart metrics.

Best SMA FinderThis script, Best SMA Finder, is a tool designed to identify the most robust simple moving average (SMA) length for a given chart, based on historical backtest performance. It evaluates hundreds of SMA values (from 10 to 1000) and selects the one that provides the best balance between profitability, consistency, and trade frequency.

What it does:

The script performs individual backtests for each SMA length using either "Long Only" or "Buy & Sell" logic, as selected by the user. For each tested SMA, it computes:

- Total number of trades

- Profit Factor (total profits / total losses)

- Win Rate

- A composite Robustness Score, which integrates Profit Factor, number of trades (log-scaled), and win rate.

Only SMA configurations that meet the user-defined minimum trade count are considered valid. Among all valid candidates, the script selects the SMA length with the highest robustness score and plots it on the chart.

How to use it:

- Choose the strategy type: "Long Only" or "Buy & Sell"

- Set the minimum trade count to filter out statistically irrelevant results

- Enable or disable the summary stats table (default: enabled)

The selected optimal SMA is plotted on the chart in blue. The optional table in the top-right corner shows the corresponding SMA length, trade count, Profit Factor, Win Rate, and Robustness Score for transparency.

Key Features:

- Exhaustive SMA optimization across 991 values

- Customizable trade direction and minimum trade filters

- In-chart visualization of results via table and plotted optimal SMA

- Uses a custom robustness formula to rank SMA lengths

Use cases:

Ideal for traders who want to backtest and auto-select a historically effective SMA without manual trial-and-error. Useful for swing and trend-following strategies across different timeframes.

📌 Limitations:

- Not a full trading strategy with position sizing or stop-loss logic

- Only one entry per direction at a time is allowed

- Designed for exploration and optimization, not as a ready-to-trade system

This script is open-source and built entirely from original code and logic. It does not replicate any closed-source script or reuse significant external open-source components.

Risk Reward Optimiser [ChartPrime]█ CONCEPTS

In modern day strategy optimization there are few options when it comes to optimizing a risk reward ratio. Users frequently need to experiment and go through countless permutations in order to tweak, adjust and find optimal in their data.

Therefore we have created the Risk Reward Optimizer.

The Risk Reward Optimizer is a technical tool designed to provide traders with comprehensive insights into their trading strategies.

It offers a range of features and functionalities aimed at enhancing traders' decision-making process.

With a focus on comprehensive data, it is there to help traders quickly and efficiently locate Risk Reward optimums for inbuilt of custom strategies.

█ Internal and external Signals:

The script can optimize risk to reward ratio for any type of signals

You can utilize the following :

🔸Internal signals ➞ We have included a number of common indicators into the optimizer such as:

▫️ Aroon

▫️ AO (Awesome Oscillator)

▫️ RSI (Relative Strength Index)

▫️ MACD (Moving Average Convergence Divergence)

▫️ SuperTrend

▫️ Stochastic RSI

▫️ Stochastic

▫️ Moving averages

All these indicators have 3 conditions to generate signals :

Crossover

High Than

Less Than

🔸External signal

▫️ by incorporating your own indicators into the analysis. This flexibility enables you to tailor your strategy to your preferences.

◽️ How to link your signal with the optimizer:

In order to be able to analysis your signal we need to read it and to do so we would need to PLOT your signal with a defined value

plot( YOUR LONG Condition ? 100 : 0 , display = display.data_window)

█ Customizable Risk to Reward Ratios:

This tool allows you to test seven different customizable risk to reward ratios , helping you determine the most suitable risk-reward balance for your trading strategy. This data-driven approach takes the guesswork out of setting stop-loss and take-profit levels.

█ Comprehensive Data Analysis:

The tool provides a table displaying key metrics, including:

Total trades

Wins

Losses

Profit factor

Win rate

Profit and loss (PNL)

This data is essential for refining your trading strategy.

🔸 It includes a tooltip for each risk to reward ratio which gives data for the:

Most Profitable Trade USD value

Most Profitable Trade % value

Most Profitable Trade Bar Index

Most Profitable Trade Time (When it occurred)

Position and size is adjustable

█ Visual insights with histograms:

Visualize your trading performance with histograms displaying each risk to reward ratio trade space, showing total trades, wins, losses, and the ratio of profitable trades.

This visual representation helps you understand the strengths and weaknesses of your strategy.

It offers tooltips for each RR ratio with the average win and loss percentages for further analysis.

█ Dynamic Highlighting:

A drop-down menu allows you to highlight the maximum values of critical metrics such as:

Profit factor

Win rate

PNL

for quick identification of successful setups.

█ Stop Loss Flexibility:

You can adjust stop-loss levels using three different calculation methods:

ATR

Pivot

VWAP

This allows you to align risk-reward ratios with your preferred risk tolerance.

█ Chart Integration:

Visualize your trades directly on your price chart, with each trade displayed in a distinct color for easy tracking.

When your take-profit (TP) level is reached , the tool labels the corresponding risk-reward ratio for that specific TP, simplifying trade management.

█ Detailed Tooltips:

Tooltips provide deeper insights into your trading performance. They include information about the most profitable trade, such as the time it occurred, the bar index, and the percentage gain. Histogram tooltips also offer average win and loss percentages for further analysis.

█ Settings:

█ Code:

In summary, the Risk Reward Optimizer is a data-driven tool that offers traders the ability to optimize their risk-reward ratios, refine their strategies, and gain a deeper understanding of their trading performance. Whether you're a day trader, swing trader, or investor, this tool can help you make informed decisions and improve your trading outcomes.

Customizable Non-Repainting HTF MACD MFI Scalper Bot Strategy v2Customizable Non-Repainting HTF MACD MFI Scalper Bot Strategy v2

This script was originally shared by Wunderbit as a free open source script for the community to work with. This is my second published iteration of this idea.

WHAT THIS SCRIPT DOES:

It is intended for use on an algorithmic bot trading platform but can be used for scalping and manual trading.

This strategy is based on the trend-following momentum indicator . It includes the Money Flow index as an additional point for entry.

This is a new and improved version geared for lower timeframes (15-5 minutes), but can be run on larger ones as well. I am testing it live as my high frequency trader.

HOW IT DOES IT:

It uses a combination of MACD and MFI indicators to create entry signals. Parameters for each indicator have been surfaced for user configurability.

Take profits are now trailing profits, and the stop loss is now fixed. Why? I found that the trailing stop loss with ATR in the previous version yields very good results for back tests but becomes very difficult to deploy live due to transaction fees. As you can see the average trade is a higher profit percentage than the previous version.

HOW IS MY VERSION ORIGINAL:

Now instead of using ATR stop loss, we have a fixed stop loss - counter intuitively to what some may believe this performs better in live trading scenarios since it gives the strategy room to move. I noticed that the ATR trailing stop was stopping out too fast and was eating away balance due to transaction fees.

The take profit on the other hand is now a trailing profit with a customizable deviation. This ensures that you can have a minimum profit you want to take in order to exit.

I have depracated the old ATR trailing stop as it became too confusing to have those as different options. I kept the old version for others that want to experiment with it. The source code still requires some cleanup, but its fully functional.

I added in a way to show RSI values and ATR values with a checkbox so that you can use the new an improved ATR Filter (and grab the right RSI values for the RSI filter). This will help to filter out times of very low volatility where we are unlikely to find a profitable trade. Use the "Show Data" checkbox to see what the values are on the indicator pane, then use those values to gauge what you want to filter out.

Both versions

Delayed Signals : The script has been refactored to use a time frame drop down. The higher time frame can be run on a faster chart (recommended on one minute chart for fastest signal confirmation and relay to algotrading platform.)

Repainting Issues : All indicators have been recoded to use the security function that checks to see if the current calculation is in realtime, if it is, then it uses the previous bar for calculation. If you are still experiencing repainting issues based on intended (or non intended use), please provide a report with screenshot and explanation so I can try to address.

Filtering : I have added to additional filters an ABOVE EMA Filter and a BELOW RSI Filter (both can be turned on and off)

Customizable Long and Close Messages : This allows someone to use the script for algorithmic trading without having to alter code. It also means you can use one indicator for all of your different alterts required for your bots.

HOW TO USE IT:

It is intended to be used in the 5-30 minute time frames, but you might be able to get a good configuration for higher time frames. I welcome feedback from other users on what they have found.

Find a pair with high volatility (example KUCOIN:ETH3LUSDT ) - I have found it works particularly well with 3L and 3S tokens for crypto. although it the limitation is that confrigurations I have found to work typically have low R/R ratio, but very high win rate and profit factor.

Ideally set one minute chart for bots, but you can use other charts for manual trading. The signal will be delayed by one bar but I have found configurations that still test well.

Select a time frame in configuration for your indicator calculations.

Select the strategy config for time frame (resolution). I like to use 5 and 15 minutes for scalping scenarios, but I am interested in hearing back from other community memebers.

Optimize your indicator without filters : customize your settings for MACD and MFI that are profitable with your chart and selected time frame calculation. Try different Take Profits (try about 2-5%) and stop loss (try about 5-8%). See if your back test is profitable and continue to optimize.

Use the Trend, RSI, ATR Filter to further refine your signals for entry. You will get less entries but you can increase your win ratio.

You can use the open and close messages for a platform integration, but I choose to set mine up on the destination platform and let the platform close it. With certain platforms you cannot be sure what your entry point actually was compared to Trading View due to slippage and timing, so I let the platform decide when it is actually profitable.

Limitations: this works rather well for short term, and does some good forward testing but back testing large data sets is a problem when switching from very small time frame to large time frame. For instance, finding a configuration that works on a one minute chart but then changing to a 1 hour chart means you lose some of your intra bar calclulations. There are some new features in pine script which might be able to address, this, but I have not had a chance to work on that issue.

72s Strat: Backtesting Adaptive HMA+ pt.1This is a follow up to my previous publication of Adaptive HMA+ few months ago, as a mean to provide some kind of initial backtesting tools. Which can be use to explore many possible strategies, optimise its settings to better conform user's pair/tf, and hopefully able to help tweaking your general strategy.

If you haven't read the study or use the indicator, kindly go here first to get the overall idea.

The first strategy introduce in this backtest is one most basic already described in the study; buy/sell is when movement is there and everything is on the right side; When RSI has turned to other side, we can use it as exit point (if in profit of course, else just let it hit our TP/SL, why would we exit before profit). Also, base on RSI when we make entry, we can further differentiate type of signals. --Please check all comments in code directly where the signals , entries , and exits section are.

Second additional strategy to check; is when we also use second faster Adaptive HMA+ for exit. So this is like a double orders on a signal but with different exit-rule (/more on this on snapshots below). Alternatively, you can also work the code so to only use this type of exit.

There's also an additional feature which you can enable its visuals, the Distance Zone , is to help measuring price distance to our xHMA+. It's just a simple atr based envelope really, I already put the sample code in study's comment section, but better gonna update it there directly for non-coder too, after this.

In this sample I use Lot for order quantity size just because that's what I use on my broker. Also what few friends use while we forward-testing it since the study is published, so we also checked/compared each profit/loss report by real number. To use default or other unit of measurement, change the entry code accordingly.

If you change your order size, you should also change the commission in Properties Tab. My broker commission is 5 USD per order/lot, so in there with example order size 0.1 lot I put commission 0.5$ per order (I'll put 2.5$ for 0.5 lot, 10$ for 2 lot, and so on). Crypto usually has higher charge. --It is important that you should fill it base on your broker.

SETTINGS

I'm trying to keep it short. Please explore it further again. (Beginner should also first get acquaintance with terms use here.)

ORDERS:

Base Minimum Profit Before Exit:

The number is multiplier of ongoing ATR. Means that when basic exit condition is met, algo will check whether you're already in minimum profit or not, if not, let it still run to TP or SL, or until it meets subsequent exit condition, then it will check again.

Default Target Profit:

Multiplier of ATR at signal. If reached before any eligible exit condition is met, exit TP.

Base StopLoss Point:

You can change directly in code to use other like ATR Trailing SL, fix percent SL, or whatever. In the sample, 4 options provided.

Maximum StopLoss:

This is like a safety-net, that if at some point your chosen SL point from input above happens to be exceeding this maximum input that you can tolerate, then this max point is the one will be use as SL.

Activate 2nd order...:

The additional doubling of certain buy/sell with different exits as described above. If enable, you should also set pyramiding to at least: 2. If not, it does nothing.

ADAPTIVE HMA+ PERIOD

Many users already have their own settings for these. So in here I only sample the default as first presented in the study. Make it to your adaptive.

MARKET MOVEMENT

(1) Now you can check in realtime how much slope degree is best to define your specific pair/tf is out of congestion (yellow) area. And (2) also able to check directly what ATR lengths are more suitable defining your pair's volatility.

DISTANCE ZONE

Distance Multiplier. Each pair/tf has its own best distance zone (in xHMA+ perspective). The zone also determine whether a signal should appear or not. (Or what type of signal, if you wanna go more detail in constructing your strategy)

USAGE

(Provided you already have your own comfortable settings for minimum-maximum period of Adaptive HMA+. Best if you already have backtested it manually too and/or apply as an add-on to your working strategy)

1. In our experiences, first most important to define is both elements in the Market Movement Settings . These also tend to be persistent for whole season since it's kinda describing that pair/tf overall behaviour. Don't worry if you still get a low Profit Factor here, but by tweaking you should start to see positive changes in one of Max Drawdown and Net Profit, or Percent Profitable.

2. Afterwards, find your pair/tf Distance Zone . When optimising this, what we seek is just a "not to bad" equity curves to start forming. At least Max Drawdown should lessen more. Doesn't have to be great already, but should be better, no red in Net Profit.

3. Then go manage the "Trailing Minimum Profit", TP, SL, and max SL.

4. Repeat 1,2,3. 👻

5. Manage order size, commission, and/or enable double-order (need pyramiding) if you like. Check if your equity can handle max drawdown before margin call.

6. After getting an acceptable backtest result, go to List of Trades tab and find the biggest loss or when many sequencing loss in a row happened. Click on it to go to exact point on chart, observe why the signal failed and get at least general idea how it can be prevented . The rest is yours, you should know your pair/tf more than other.

You can also re-explore your minimum-maximum period for both Major and minor xHMA+.

Keep in mind that all numbers in Setting are conceptually in a form of range . You don't want to get superb equity curves but actually a "fragile" , means one can easily turn it to disaster just by changing only a fraction in one/two of the setting.

---

If you just wanna test the strength of the indicator alone, you can disable "Use StopLoss" temporarily while optimising settings.

Using no SL might be tempting in overall result data in some cases, but NOTE: It is not recommended to not using SL, don't forget that we deliberately enter when it's in high volatility. If want to add flexibility or trading for long-term, just maximise your SL. ie.: chose SL Point>ATR only and set it maximum. (Check your max drawdown after this).

I think this is quite important specially for beginners, so here's an example; Hypothetically in below scenario, because of some settings, the buy order after the loss sell signal didn't appear. Let's say if our initial capital only 1000$ using leverage and order size 0,5 lot (risky position sizing already), moreover if this happens at the beginning of your trading season, that's half of account gone already in one trade . Your max SL should've made you exit after that pumping bar.

The Trailing Minimum Profit is actually look like this. Search in the code if you want to plot it. I just don't like too many lines on chart.

To maximise profit we can try enabling double-order. The only added rule coded is: RSI should rising when buy and falling when sell. 2nd signal will appears above or below default buy/sell signal. (Of course it's also prone to double-loss, re-check your max drawdown after. Profit factor play its part in here for a long run). Snapshot in comparison:

Two default sell signals on left closed at RSI exit, the additional sell signal closed later on when price crossover minor xHMA+. On buy side, price haven't met our minimum profit when first crossunder minor xHMA+. If later on we hit SL on this "+buy" signal, at least we already profited from default buy signal. You can also consider/treat this as multiple TP points.

For longer-term trading, what you need to maximise is the Minimum Profit , so it won't exit whenever an exit condition happened, it can happen several times before reaching minimum profit. Hopefully this snapshot can explain:

Notice in comparison default sell and buy signal now close in average after 3 days. What's best is when we also have confirmation from higher TF. It's like targeting higher TF by entering from smaller TF.

As also mention in the study, we can still experiment via original HMA by putting same value for minimum-maximum period setting. This is experimental EU 1H with Major xHMA+: 144-144, Flat market 13, Distance multiplier 3.6, with 2nd order activated.

Kiwi was a bit surprising for me. It's flat market is effectively below 6, with quite far distance zone of 3.5. Probably because I'm using big numbers in adaptive period.

---

The result you see in strategy tester report below for EURUSD 15m is using just default settings you see in code, as follow:

0,1 lot for each order (which is the smallest allowed by my broker).

No pyramiding. Commission: 0.5 usd per order. Slippage: 3

Opening position is only using basic strategy #1 (RSI exit). Additional exit not activated.

Minimum Profit: 1. TP: 3.

SL use: Half-distance zone. Max SL: 4.5.

Major xHMA+: 172-233. minor xHMA+: 89-121

Distance Zone Multiplier: 2.7

RSI: Standard 14.

(From our forward-testing, the difference we get from net profit is because of the spread, our entry isn't exactly at the close/open price. Not so much though, but not the same. If somebody can direct me to any example where we can code our entry via current bid/ask price, that would be awesome!)

It's already a long post (sorry), think I'm gonna pause here. Check out the code :)

---

DISCLAIMER: Past performance is no guarantee of future results , and so on.. you know the drill ;)

Please read whole description first before using, don't take 1-2 paragraph and claim it's the whole logic, you are responsible of your own actions and understanding.

EMA Crossover StrategyEMA Crossover Strategy

This strategy will enter a long trade when the 21 EMA crosses over the 55 EMA and both EMAs and the close price are above the 200 EMA (long-term trend).

It will enter a short trade when the 21 EMA crosses under the 55 EMA and both EMAs and the close price are below the 200 EMA.

It will exit a long trade when the RSI crosses under from overbought and indicates that the uptrend could be coming to an end.

It will exit a short trade when the RSI crosses over from oversold and indicates that the downtrend could be coming to an end.

Backtesting shows that it works best on:

30 MIN:

SYMBOL - PROFIT FACTOR

AUDCAD - 1.126

EURJPY - 1.12

EURNZD - 1.04

EURUSD - 1.65

GBPAUD - 1.27

USDCAD - 1.08

1 HR:

SYMBOL - PROFIT FACTOR

CADJPY- 1.23

EURNZD- 1.166

GBPJPY- 1.23

GBPUSD- 1.282

NZDJPY- 1.246

USDCHF- 1.344

3 HR:

SYMBOL - PROFIT FACTOR

CADCHF- 1.975

EURGBP- 1.776

EURNZD- 1.911

GBPAUD- 1.364

GBPCHF- 1.311

USDJPY- 1.162

XAUUSD - 2.00

As always, this strategy does not guarantee you to achieve profits and you should always use confirmations before entering a trade.

Adaptive Trend SelectorThe Adaptive Trend Selector is a comprehensive trend-following tool designed to automatically identify the optimal moving average crossover strategy. It features adjustable parameters and an integrated backtester that delivers institutional-grade insights into the recommended strategy. The model continuously adapts to new data in real time by evaluating multiple moving average combinations, determining the best performing lengths, and presenting the backtest results in a clear, color-coded table that benchmarks performance against the buy-and-hold strategy.

At its core, the model systematically backtests a wide range of moving average combinations to identify the configuration that maximizes the selected optimization metric. Users can choose to optimize for absolute returns or risk-adjusted returns using the Sharpe, Sortino, or Calmar ratios. Alternatively, users can enable manual optimization to test custom fast and slow moving average lengths and view the corresponding backtest results. The label displays the Compounded Annual Growth Rate (CAGR) of the strategy, with the buy-and-hold CAGR in parentheses for comparison. The table presents the backtest results based on the fast and slow lengths displayed at the top:

Sharpe = CAGR per unit of standard deviation.

Sortino = CAGR per unit of downside deviation.

Calmar = CAGR relative to maximum drawdown.

Max DD = Largest peak-to-trough decline in value.

Beta (β) = Return sensitivity relative to buy-and-hold.

Alpha (α) = Excess annualized risk-adjusted returns.

Win Rate = Ratio of profitable trades to total trades.

Profit Factor = Total gross profit per unit of losses.

Expectancy = Average expected return per trade.

Trades/Year = Average number of trades per year.

This indicator is designed with flexibility in mind, enabling users to specify the start date of the backtesting period and the preferred moving average strategy. Supported strategies include the Exponential Moving Average (EMA), Simple Moving Average (SMA), Wilder’s Moving Average (RMA), Weighted Moving Average (WMA), and Volume-Weighted Moving Average (VWMA). To minimize overfitting, users can define constraints such as a minimum and maximum number of trades per year, as well as an optional optimization margin that prioritizes longer, more robust combinations by requiring shorter-length strategies to exceed this threshold. The table follows an intuitive color logic that enables quick performance comparison against buy-and-hold (B&H):

Sharpe = Green indicates better than B&H, while red indicates worse.

Sortino = Green indicates better than B&H, while red indicates worse.

Calmar = Green indicates better than B&H, while red indicates worse.

Max DD = Green indicates better than B&H, while red indicates worse.

Beta (β) = Green indicates better than B&H, while red indicates worse.

Alpha (α) = Green indicates above 0%, while red indicates below 0%.

Win Rate = Green indicates above 50%, while red indicates below 50%.

Profit Factor = Green indicates above 2, while red indicates below 1.

Expectancy = Green indicates above 0%, while red indicates below 0%.

In summary, the Adaptive Trend Selector is a powerful tool designed to help investors make data-driven decisions when selecting moving average crossover strategies. By optimizing for risk-adjusted returns, investors can confidently identify the best lengths using institutional-grade metrics. While results are based on the selected historical period, users should be mindful of potential overfitting, as past results may not persist under future market conditions. Since the model recalibrates to incorporate new data, the recommended lengths may evolve over time.

AlgoWay GRSIM🧭 What this strategy tries to do

This strategy detects when a market move is losing strength and prepares for a potential reversal, but it waits for fresh momentum confirmation before acting.

It combines:

• RSI-based divergence (to spot exhaustion and potential turning points),

• Impulse MACD (to verify that the new direction actually has force behind it).

________________________________________

⚙️ When it takes trades

Long (Buy):

• A bullish RSI divergence appears (a clue that selling pressure is fading);

• Within a short time window, the Impulse MACD turns strongly positive;

• Optionally, the impulse line itself must be rising (if the Impulse Direction Filter is

enabled).

Short (Sell):

• A bearish RSI divergence appears (buying pressure fading);

• Within a short time window, the Impulse MACD turns strongly negative;

• Optionally, the impulse line must be falling (if the Impulse Direction Filter is enabled).

If momentum confirmation happens too late, the divergence “expires” and the signal is ignored.

________________________________________

🧩 How entries work

1. Reversal clue:

The strategy detects disagreement between price and RSI (price makes a new high/low, RSI doesn’t).

That suggests a shift in underlying strength.

2. Momentum confirmation:

Before entering, the Impulse MACD must agree — showing real push in the same direction.

3. Impulse direction filter (optional):

When enabled, the impulse itself must accelerate (rise for longs, fall for shorts), avoiding fake signals where price diverges but momentum is still fading.

4. No stacking:

It opens only one position at a time.

________________________________________

🚪 How exits work

Two main exit styles:

Conservative (default):

Longs close when impulse crosses below its signal line.

Shorts close when impulse crosses above its signal line.

✅ Keeps trades as long as momentum agrees.

Color-change (fast):

Longs close immediately when impulse flips bearish.

Shorts close immediately when impulse flips bullish.

⚡ Faster and more defensive.

Plus:

Stop Loss (%) and Take Profit (%) act as fixed-distance protective exits (set to 0 to disable either one).

________________________________________

📊 What you’ll see on the chart

A thick Impulse MACD line and thin signal line (oscillator view).

Diamonds — detected bullish/bearish divergence points.

Circles — where impulse crosses its signal (momentum change).

A performance panel (top-right) showing Net Profit, Trades, Win Rate, Profit Factor, Pessimistic PF, and Max Drawdown.

________________________________________

🔧 What you can tune

Signal Lifetime (bars): how long a divergence remains valid.

Impulse Direction Filter: ensure the impulse itself is moving in the trade’s direction.

Stop Loss / Take Profit (%): risk and target in percent.

Exit Style: conservative cross or faster color-change.

RSI / MA / Signal Lengths: adjust responsiveness (defaults are balanced).

________________________________________

💪 Strengths

Confirms reversals using momentum direction, not just divergence.

Avoids “early” signals where momentum is still fading.

Works symmetrically for longs and shorts.

Built-in stop/target protection.

Clear, visual confirmation of all logic components.

________________________________________

⚠️ Things to keep in mind

In sideways markets, the impulse can flip often — prefer conservative exits.

Too small SL/TP → constant stop-outs.

Too wide SL/TP → deep drawdowns.

Always test with different timeframes and markets.

________________________________________

💡 Practical tips

Start with default settings.

Enable “Use Impulse Direction Filter” in trending markets, disable it in very choppy ones.

Focus on Profit Factor, Win Rate, and Max Drawdown after several dozen trades.

Keep SL/TP roughly aligned with typical swing size.

“AlgoWay GRSIM” is a reversal-with-confirmation strategy: it spots likely turns, demands real momentum alignment (optionally verified by impulse direction), and manages exits with clear momentum cues plus built-in protective limits.

Adaptive Trend Breaks Adaptive Trend Breaks

## WHAT IT DOES

This script is a modified and enhanced version of "Trendline Breakouts With Targets" concept by ChartPrime.

Adaptive Trend Breaks (ATB) is a trendline breakout system optimized for scalping liquid futures contracts. The indicator automatically draws dynamic support and resistance trendlines based on pivot points, then generates trade signals when price breaks through these levels with confirmation filters. It includes automated target and stop-loss placement with real-time P&L tracking in dollars.

## HOW IT WORKS

**Trendline Detection Method:**

The indicator uses pivot high/low detection to identify significant price turning points. When a new pivot forms, it calculates the slope between consecutive pivots to draw dynamic trendlines. These lines extend forward based on the established trend angle, creating actionable support and resistance zones.

**Band System:**

Around each trendline, the script creates a "band" using a volatility-adjusted calculation: `ATR(14) * 0.2 * bandwidth multiplier / 2`. This adaptive band accounts for current market conditions - wider during volatile periods, tighter during quiet markets.

**Breakout Logic:**

A breakout signal triggers when:

1. Price closes beyond the trendline + band zone

2. Volume exceeds the 20-period moving average by your set multiplier (default 1.2x)

3. Price is within Regular Trading Hours (9:30-16:00 EST) if session filter enabled

4. Current ATR meets minimum volatility threshold (prevents trading dead markets)

**Target & Stop Calculation:**

Upon breakout confirmation:

- **Entry**: Trendline breach point

- **Target**: Entry ± (bandwidth × target multiplier) - default 8x for quick scalps

- **Stop**: Entry ± (bandwidth × stop multiplier) - default 8x for 1:1 risk/reward

- Multipliers adjust automatically to market volatility through the ATR-based band

**P&L Conversion:**

The script converts point movements to dollars using:

```

Dollar P&L = (Price Points × Contract Point Value × Quantity)

```

For example, a 10-point NQ move with 2 contracts = 10 × $20 × 2 = $400

## HOW TO USE IT

**Setup:**

1. Select your instrument (NQ/ES/YM/RTY) - point values auto-configure

2. Set contract quantity for accurate dollar P&L

3. Choose pivot period (lower = more signals but more noise, default 5 for scalping)

4. Adjust bandwidth multiplier if trendlines are too tight/loose (1-5 range)

**Filters Configuration:**

- **Volume Filter**: Requires breakout volume > moving average × multiplier. Increase multiplier (1.5-2.0) for higher conviction trades

- **Session Filter**: Enable to trade only RTH. Disable for 24-hour trading

- **ATR Filter**: Prevents signals during low volatility. Increase minimum % for more active markets only

**Risk Management:**

- Set target/stop multipliers based on your risk tolerance

- 8x bandwidth = approximately 1:1 risk/reward for most liquid futures

- Enable trailing stops for trend-following approach (moves stop to protect profits)

- Adjust line length to see targets further into the future

**Statistics Table:**

- Choose timeframe to analyze: all-time, today, this week, custom days

- Monitor win rate, profit factor, and net P&L in dollars

- Track long vs short performance separately

- See real-time unrealized P&L on active trades

**Reading Signals:**

- **Green triangle below bar** = Long breakout (resistance broken)

- **Red triangle above bar** = Short breakout (support broken)

- **White dashed line** = Entry price

- **Orange line** = Take profit target with dollar value

- **Red line** = Stop loss with dollar value

- **Green checkmark (✓)** = Target hit, winning trade

- **Red X (✗)** = Stop hit, losing trade

## WHAT IT DOES NOT DO

**Limitations to Understand:**

- Does not predict future trendline formations - it reacts to breakouts after they occur

- Historical trendlines disappear after breakout (not kept on chart for clarity)

- Requires sufficient volatility - may not signal in extremely quiet markets

- Volume filter requires exchange volume data (not available on all symbols)

- Statistics are indicator-based simulations, not actual trading results

- Does not account for slippage, commissions, or order fills

## BEST PRACTICES

**Recommended Settings by Market:**

- **NQ (Nasdaq)**: Default settings work well, consider volume multiplier 1.3-1.5

- **ES (S&P 500)**: Slightly slower, try period 7-8, volume 1.2

- **YM (Dow)**: Lower volatility, reduce bandwidth to 1.5-2

- **RTY (Russell)**: Higher volatility, increase bandwidth to 3-4

**Risk Management:**

- Never risk more than 2-3% of account per trade

- Use contract quantity calculator: Max Risk $ ÷ (Stop Distance × Point Value)

- Start with 1 contract while learning the system

- Backtest your specific timeframe and instrument before live trading

**Optimization Tips:**

- Increase pivot period (7-10) for fewer but higher-quality signals

- Raise volume multiplier (1.5-2.0) in choppy markets

- Lower target/stop multipliers (5-6x) for tighter profit taking

- Use trailing stops in strong trending conditions

- Disable session filter for overnight gaps and Asia session moves

## TECHNICAL DETAILS

**Key Calculations:**

- Pivot Detection: `ta.pivothigh(high, period, period/2)` and `ta.pivotlow(low, period, period/2)`

- Slope Calculation: `(newPivot - oldPivot) / (newTime - oldTime)`

- Adaptive Band: `min(ATR(14) * 0.2, close * 0.002) * multiplier / 2`

- Breakout Confirmation: Price crosses trendline + 10% of band threshold

**Data Requirements:**

- Minimum bars in view: 500 for proper pivot calculation

- Volume data required for volume filter accuracy

- Intraday timeframes recommended (1min - 15min) for scalping

- Works on any timeframe but optimized for fast execution

**Performance Metrics:**

All statistics calculate based on indicator signals:

- Tracks every signal as a trade from entry to TP/SL

- P&L in actual contract dollar values

- Win rate = (Winning trades / Total trades) × 100

- Profit factor = Gross profit / Gross loss

- Separates long/short performance for bias analysis

## IDEAL FOR

- Futures scalpers and day traders

- Traders who prefer visual trendline breakouts

- Those wanting automated TP/SL placement

- Traders tracking performance in dollar terms

- Multiple timeframe analysis (compare 1min vs 5min signals)

## NOT SUITABLE FOR

- Swing trading (targets too close)

- Stocks/forex without modifying point values

- Extremely low timeframes (<30 seconds) - too much noise

- Markets without volume data if using volume filter

- Illiquid contracts (signals may not execute at shown prices)

---

**Settings Summary:**

- Core: Period, bandwidth, extension, trendline style

- Filters: Volume, RTH session, ATR volatility

- Risk: R:R ratio, target/stop multipliers, trailing stop

- Display: Stats table position, size, colors

- Stats: Timeframe selection (all-time to custom days)

**License:** This indicator is published open-source under Mozilla Public License 2.0. You may use and modify the code with proper attribution.

**Disclaimer:** This indicator is for educational purposes. Past performance does not guarantee future results. Always practice proper risk management and test thoroughly before live trading.

---

## CREDITS & ATTRIBUTION

This script builds upon the "Trendline Breakouts With Targets" concept by ChartPrime with significant enhancements:

**Major Improvements Added:**

- **Futures-Specific Calculations**: Automated dollar P&L conversion using actual contract point values (NQ=$20, ES=$50, YM=$5, RTY=$50)

- **Advanced Statistics Engine**: Comprehensive performance tracking with customizable timeframe analysis (today, week, month, custom ranges)

- **Multi-Layer Filtering System**: Volume confirmation, RTH session filter, and ATR volatility filter to reduce false signals

- **Professional Trade Management**: Enhanced visual trade tracking with separate TP/SL lines, dollar value labels, and optional trailing stops

- **Optimized for Scalping**: Faster pivot periods (5 vs 10), tighter bands, and reduced extension bars for quick entries

Original trendline detection methodology by ChartPrime - used with modification under Mozilla Public License 2.0.

Candlestick Patterns Backtester [Optimized]Candlestick Patterns Backtester

What this is: This indicator is based on a really cool candlestick pattern backtester that I found (I'll update this later when I remember where I got it from or find the actual author). The original had this massive table showing win/loss ratios for a bunch of candlestick patterns, and according to the built-in backtester, it was actually profitable - which was pretty impressive.

The Problem: I played around with the original for a while but honestly wasn't really able to get it to work well at all for actual trading. It was still pretty cool to look at though! The main issues were:

It was just a big static table - hard to do anything useful with it

Couldn't send signals out to other strategies

The code was a monster - like 2,000+ lines of repetitive mess

What I Did: I completely refactored this thing and got it down from 2,000+ lines to just a few hundred lines. Much cleaner now! Here's what it does:

45+ Candlestick Patterns - All the classics are in there

Dynamic Filtering - Set your own requirements (minimum win rate, profit factor, total trades, etc.)

Flexible Logic - Choose AND/OR logic for your filters

Signal Generation - Creates actual buy/sell signals you can use with other strategies

Visual Badges - Shows pattern badges on chart when they meet your criteria

Active Patterns Table - Only shows patterns that are currently profitable based on your settings

Settings You Can Adjust:

Minimum win rate threshold

Minimum profit factor

Minimum number of trades required

Whether to use AND or OR logic for filtering

Colors, badge display, debug options

Reality Check: Trading these patterns really wasn't for me, but it was still a great learning experience. The backtesting results look good on paper, but as always, past performance doesn't guarantee future results. Use this as a research tool and educational resource more than anything else.

Credit: This is based on someone else's original work that I heavily modified and optimized. I'll update this description once I track down the original author to give proper credit where it's due.

This introduction captures your casual, honest tone while explaining the technical improvements you made and setting realistic expectations about the indicator's practical use.

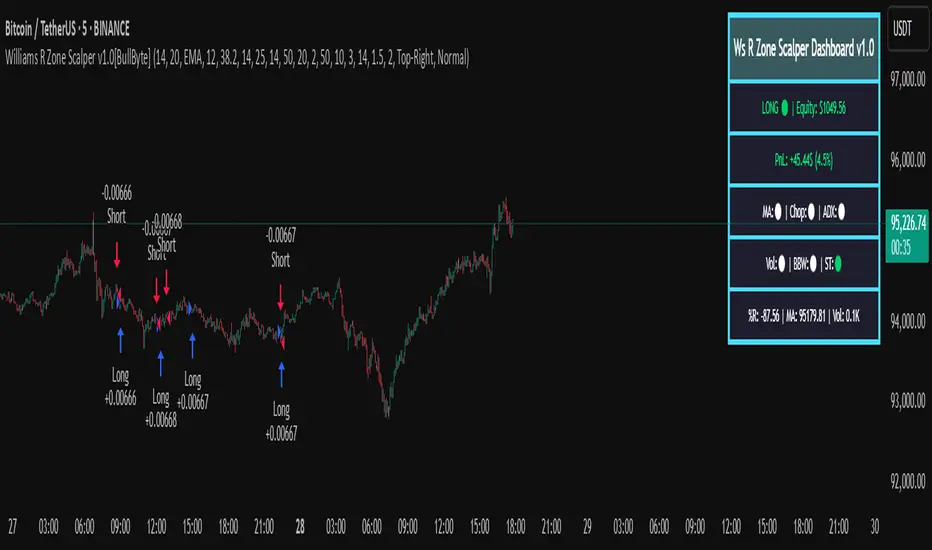

Williams R Zone Scalper v1.0[BullByte]Originality & Usefulness

Unlike standard Williams R cross-over scripts, this strategy layers five dynamic filters—moving-average trend, Supertrend, Choppiness Index, Bollinger Band Width, and volume validation —and presents a real-time dashboard with equity, PnL, filter status, and key indicator values. No other public Pine script combines these elements with toggleable filters and a custom dashboard. In backtests (BTC/USD (Binance), 5 min, 24 Mar 2025 → 28 Apr 2025), adding these filters turned a –2.09 % standalone Williams R into a +5.05 % net winner while cutting maximum drawdown in half.

---

What This Script Does

- Monitors Williams R (length 14) for overbought/oversold reversals.

- Applies up to five dynamic filters to confirm trend strength and volatility direction:

- Moving average (SMA/EMA/WMA/HMA)

- Supertrend line

- Choppiness Index (CI)

- Bollinger Band Width (BBW)

- Volume vs. its 50-period MA

- Plots blue arrows for Long entries (R crosses above –80 + all filters green) and red arrows for Short entries (R crosses below –20 + all filters green).

- Optionally sets dynamic ATR-based stop-loss (1.5×ATR) and take-profit (2×ATR).

- Shows a dashboard box with current position, equity, PnL, filter status, and real-time Williams R / MA/volume values.

---

Backtest Summary (BTC/USD(Binance), 5 min, 24 Mar 2025 → 28 Apr 2025)

• Total P&L : +50.70 USD (+5.05 %)

• Max Drawdown : 31.93 USD (3.11 %)

• Total Trades : 198

• Win Rate : 55.05 % (109/89)

• Profit Factor : 1.288

• Commission : 0.01 % per trade

• Slippage : 0 ticks

Even in choppy March–April, this multi-filter approach nets +5 % with a robust risk profile, compared to –2.09 % and higher drawdown for Williams R alone.

---

Williams R Alone vs. Multi-Filter Version

• Total P&L :

– Williams R alone → –20.83 USD (–2.09 %)

– Multi-Filter → +50.70 USD (+5.05 %)

• Max Drawdown :

– Williams R alone → 62.13 USD (6.00 %)

– Multi-Filter → 31.93 USD (3.11 %)

• Total Trades : 543 vs. 198

• Win Rate : 60.22 % vs. 55.05 %

• Profit Factor : 0.943 vs. 1.288

---

Inputs & What They Control

- wrLen (14): Williams R look-back

- maType (EMA): Trend filter type (SMA, EMA, WMA, HMA)

- maLen (20): Moving-average period

- useChop (true): Toggle Choppiness Index filter

- ciLen (12): CI look-back length

- chopThr (38.2): CI threshold (below = trending)

- useVol (true): Toggle volume-above-average filter

- volMaLen (50): Volume MA period

- useBBW (false): Toggle Bollinger Band Width filter

- bbwMaLen (50): BBW MA period

- useST (false): Toggle Supertrend filter

- stAtrLen (10): Supertrend ATR length

- stFactor (3.0): Supertrend multiplier

- useSL (false): Toggle ATR-based SL/TP

- atrLen (14): ATR period for SL/TP

- slMult (1.5): SL = slMult × ATR

- tpMult (2.0): TP = tpMult × ATR

---

How to Read the Chart

- Blue arrow (Long): Williams R crosses above –80 + all enabled filters green

- Red arrow (Short) : Williams R crosses below –20 + all filters green

- Dashboard box:

- Top : position and equity

- Next : cumulative PnL in USD & %

- Middle : green/white dots for each filter (green=passing, white=disabled)

- Bottom : Williams R, MA, and volume current values

---

Usage Tips

- Add the script : Indicators → My Scripts → Williams R Zone Scalper v1.0 → Add to BTC/USD chart on 5 min.

- Defaults : Optimized for BTC/USD.

- Forex majors : Raise `chopThr` to ~42.

- Stocks/high-beta : Enable `useBBW`.

- Enable SL/TP : Toggle `useSL`; stop-loss = 1.5×ATR, take-profit = 2×ATR apply automatically.

---

Common Questions

- * Why not trade every Williams R reversal?*

Raw Williams R whipsaws in sideways markets. Choppiness and volume filters reduce false entries.

- *Can I use on 1 min or 15 min?*

Yes—adjust ATR length or thresholds accordingly. Defaults target 5 min scalping.

- *What if all filters are on?*

Fewer arrows, higher-quality signals. Expect ~10 % boost in average win size.

---

Disclaimer & License

Trading carries risk of loss. Use this script “as is” under the Mozilla Public License 2.0 (mozilla.org). Always backtest, paper-trade, and adjust risk settings to your own profile.

---

Credits & References

- Pine Script v6, using TradingView’s built-in `ta.supertrend()`.

- TradingView House Rules: www.tradingview.com

Goodluck!

BullByte

Divergence IQ [TradingIQ]Hello Traders!

Introducing "Divergence IQ"